Published 12/05/2026

When it comes to short-run economic management, we are still using a toolkit built for the 1990s. During that Great Moderation, all governments and central banks had to do was to fine-tune strong, stable economies. But history did not end there. In fact, rather a lot of history has been happening.

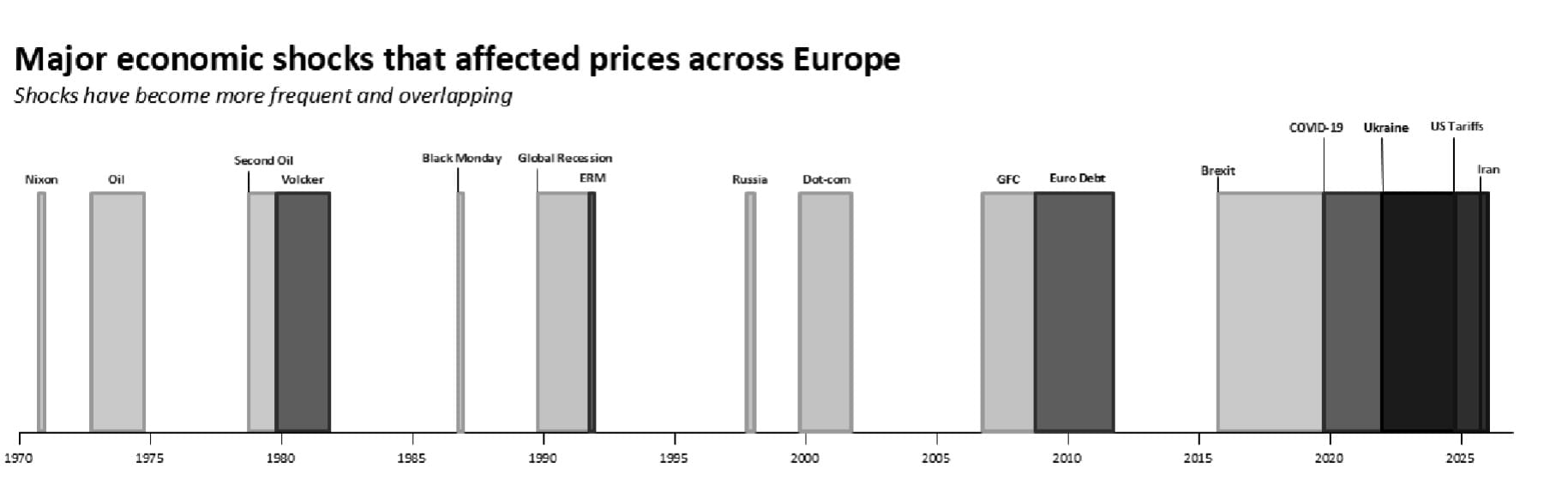

Global shocks affecting prices have come with increasing frequency since the 2008 Global Financial Crisis. Unsurprisingly, incumbent governments around the world have suffered the results. Over the past fifteen years, central banks have proven unable to raise demand sufficiently during austerity when the economy was underheating, while also proving unable to control inflation when the economy was overheating.

Figure 1: Timeline of Economic Shocks. Major economic shocks which changed prices from 1971–2026. Bar width indicates persistence of price shocks and bars darken where crises coincide. Based on IMF Regional European Outlook 2026.

Our country’s response to the first problem is now widely accepted as having failed: against the efforts of the central bank, the Tory-Lib Dem austerity government put the brakes on demand in the 2010s. Our response to the second problem needs to be informed by that failure.

Central banks cannot tackle external price shocks alone. Governments need to step up and take an active role in price stabilisation by developing policy levers to productively shape the economy, improve our resilience and reduce our exposure to global shocks. Much as central banks do, the Treasury should improve its monitoring of supply chains to help it intervene early when prices rise – and make more use of the intelligence gathered by the Bank of England. Our target should be a low-inflation, low-interest rates, high-investment economy.

This does not mean closing us off from international trade; on the contrary, the Labour Government’s reset of relations with the European Union, and its talks to conclude an agrifood deal, are extremely necessary. Instead, it means understanding the geopolitics of our trading blocs, and working on our vulnerabilities, such as energy import dependence.

Expanding the supply-side capacity of an economy is a notoriously long-term feat. Roads and railways take time to plan and build. While the UK has obvious regional and urban-rural inequalities, unleashing the catch-up growth from resolving these will take years.

When it comes to long-run economic policy, the old Washington Consensus has been roundly discredited. The Biden Administration in the US embraced interventionist industrial strategy. Earlier this year, the World Bank itself admitted that industrial policy can and does affect long-run growth.1 Without a more active state, the UK risks remaining stuck in a ‘low growth trap’ caused by ‘a three-decade period of ultra-low investment’.2

While the UK centre-left have recognised this for some time, we haven’t fully spelt out what it means for the state’s role in the economy. We need an agile state: one that recognises the productive capacity in the economy and expands it by being a ‘market shaper’, in Mariana Mazzucato’s terminology.

While the previous chapter focused on the demand side and the cost of living, this one will broadly look at the supply side and growth.

Investment

Investment is the factor of production that changes the most quickly. In addition, there is some consensus that underinvestment is largely responsible for the growth doom loop the UK has been stuck in.3 In her 2026 Mais lecture, the Chancellor said: ‘the object is to turn around our medium-run productivity performance, and build an investment-led growth model for the UK’.

Yet raising investment does not mean courting any and all investors that come our way. Ownership matters, because ownership determines costs and governance styles. It makes a difference to our citizens whether our nurseries, football clubs and water companies are owned by foreign private equity consortiums, compared to local residents, co-operatives or non-profit public interest corporations.

Therefore, the state should not be agnostic in tilting the playing field towards styles of ownership with stronger public benefits. The Government already recognises this in part, with its commitment to doubling the size of the co-operative and mutual economy.

1. Private investment

Although UK private returns are high, and higher than our European peers, private sector investment has been disappointing – analysis shows the UK ranks twenty-eighth for business investment out of thirty-one OECD countries.4

The fall in private investment fall started in the early 2000s, long before policy instability rocked the country. Part of the explanation is ownership. Companies run on a short-term profit motive by distant owners, particularly private equity, often don’t invest for the long term. This includes the private funds that buy up our utilities, housing and services, are often focussed on cutting costs at the expense of investment and service quality. In some sectors, they can get away with doing so because they have a captive market with near-guaranteed returns.

When the people who are most affected by low investment levels – workers – get a say in a company’s governance then investment levels go up, as evidenced in Germany.5 Economists studying the impact of the German reforms say that ‘shared governance may crowd in investment […] either by facilitating cooperation, by institutionalizing communication, or through repeated interactions between labor and capital’.6 In other words, higher levels of worker bargaining power affects not just wages, but also investment.

As the Resolution Foundation writes: ‘Where Britain stands out is the unusual lack of pressure on managers from above – via engaged owners – or below – from empowered workers – to invest for long term growth. A smaller number of larger, and more active, pension funds is what UK PLC needs, along with worker representatives on large firms’ boards’.7

Pro-growth tax reforms that boost investment include moving to a fairer property tax, introducing an investment allowance to stop the taxing of inflationary gains, and tightening controls on capital leakage.8 These measures are discussed in more depth elsewhere in this collection.

2. Public investment

High and volatile prices for government debt are constraining the Treasury’s ability to borrow to invest. But that does not mean taxation is the only route to higher public investment. When comparing the UK’s public investment levels with higher-achieving peers, what stands out is the lack of a powerful policy bank that can produce stable, long-term investment plans beyond the political cycle, surviving austerity-loving governments.

The Government’s new investment vehicle, the National Wealth Fund, does not have the size of balance sheet to make enough of a dent in the problem of growth. That is because, as the Treasury Select Committee’s inquiry notes, it is ‘financed by taxation and borrowing, which means its investments are likely to attract public, political and media scrutiny’.9

Instead of keeping vehicles like the NWF on the Government’s balance sheet indefinitely, they should be made to earn their own keep and issue their own debt, much as the French and German policy banks do. Such financial independence would not only enable them to expand the quantum of their investment, it would also allow them to take riskier, longer-term bets that don’t need to pay off within a five-year Parliament. In the New Economics Foundation (NEF)’s submission to the Treasury Committee:

Currently, the NWF’s total planned investment capacity of £27.8bn over nine years is trifling compared to the volumes invested by policy banks in comparable countries. The French Banque Publique d’Investissement (Bpifrance) and german Kreditanstalt für Wiederaufbau (KfW) each invest roughly 1 per cent of their country’s gross domestic product (GDP) annually. If the UK did the same, that would imply the NWF investing £21bn per year by 2028 – 29, almost four times its current investment limit.10

More broadly, there are many productive infrastructure projects available in the UK that could be owned by public corporations. These public corporations can be run not for profit by an independent executive that aligns with a long-run government strategy. They need permission to cut through the kind of red tape the government has already been removing from planning.

Such bodies can include development corporations, which can internalise the benefits of building infrastructure and housing by owning the land around their projects, and thus profiting from higher house prices in the areas they improve.

Labour market reform

Within the short-run business cycle, the UK labour market is currently loosening, with a higher number of jobseekers per vacancy. Therefore increasing labour supply has to go in tandem with increasing jobs and training opportunities; the sequencing of measures matters.

Labour supply matters across the income distribution. Tax reforms are needed to tackle the cliff edges both at the top and bottom income bands.11This tends to hurt low-income households, while high income households reduce their hours to avoid rolling off the cliff. This hurts productivity and tax take.

1. Childcare and parental leave

Childcare is both an essential and unavoidable cost for working families, as well as a significant determinant of labour supply (the OBR said that the expansion of childcare entitlements announced in 2023 would result an increase in labour market participation of parents of young children by 60,000).12 Thus it is a doubly important cost for the government to tackle.

The Government has doubled childcare provision from 15 to 30 hours for eligible working parents – saving parents up to £7,500 a year.13 Yet families in the UK still face some of the highest childcare costs in the OECD, because of a lack of public investment, high demand and low supply of childcare workers.14

The OECD estimates that working couples in the UK allocate up to a third of their post-tax income to full time childcare for two children. In Sweden, the OECD puts the net cost of childcare for a similar family at 5 per cent of income, a fifth as much as the UK.15

The fact that it is mostly mothers who stay home points to a solution that is both feminist and progressive: enabling men to parent. Statutory Paternity Pay replaces around 33 per cent for an employee father on median income, while offering two weeks of leave. By comparison on average OECD countries offer 8.1 weeks of leave at full pay.16

This poor offer produces severely unequal outcome. 60 per cent of those claiming shared parental leave are in the top 20 per cent of earners, while the bottom half of earners made just 5 per cent of claims.17

JRF estimates that the most notable growth impacts would come if the government offered men six weeks of parental leave at 90 per cent of their average weekly pay, capped at £1,200 – similar to the existing six-week offer for women.18 This would cost £1.1bn in gross terms, but generate enough tax revenue from women returning to work to only cost £220mn in net terms – with even bigger economy-wide benefits dwarfing the costs.

A cap on childcare costs at 5 per cent of household earnings would be progressive and would incentivise parents to work more hours – as their childcare costs would rise at a manageable rate as their income goes up.19 Depending on behavioural response, this would be essentially cost neutral.

2. Social security reform

The social security system, as currently constructed, doesn’t allow for the flexible transitions a dynamic economy requires between work and re-training, and between jobs in different sectors.

The labour market will continue to struggle without action. Unemployment insurance and a retraining offer will help deal with the disruption of AI. We should also consider proposals for a baseline level of social security.20

Because the current system focuses solely on getting people into work at the earliest opportunity, it doesn’t match people with jobs they are likely to stay and grow in long-term, thus trapping people in low-productivity positions and making it more likely they lose or quit their jobs once more.

We know that relational work coaching improves pay and career progression – which is one reason this government has ramped up the number of Work Coaches to provide tailored and personalised support.21

Adapting key features of the Danish or Swedish style flexicurity models would improve macroeconomic stabilisation. Under such a system, workers are more likely to take risks and change jobs in order to progress their careers. Most people are likely to dip in and out of social security once or twice throughout their working age life – gaining the flexibility to do so on their own terms, rather than the employer’s terms.

Trade unions would take a much more comprehensive role in setting wages and conditions through sector-wide bargaining, as well as determining the kinds of training to be funded.

The Scandinavian models have been co-produced with labour unions and employer associations. It is important that reforms build on our landmark Employment Rights Act and are developed in consultation with workers and their union representatives.

Higher economic security makes for a more dynamic economy.22 On the flipside, economic insecurity makes individuals and households less likely to take productivity-increasing job moves, and also makes it less likely that individuals will start their own business.

Economic dynamism and regulation

Turning to regulation, David Cameron’s government created a one in, one out rule for new regulations to encourage the civil service to cut red tape. By 2016 this became one in, three out – a rule that has been directly linked to the Grenfell Tower fire in 2017.

Cutting red tape in this manner is not only overly simplistic, but also dangerous. Instead, we need smarter, stronger and simpler regulation, not fewer or more regulatory processes. In some areas, regulators have failed companies, creating an uncertain investment climate – whereas in others, regulators have failed consumers. Both can be true at the same time.

To increase economic dynamism, we need an understanding not only of the sectors and behaviours that we wish to encourage, as set out in the Government’s industrial strategy. We also need to lay out what kinds of corporate behaviour we stand against, such as rip-off and zombie firms. Regulators like the Competition and Markets Authority both need to be streamlined, so they come to decisions more quickly and apply clearer criteria, but also empowered to crack down on rip-offs.

This is a process that will take time. In the meantime, in some areas with high growth potential, we should look at special channels for lightening the regulatory burden.

For example, the lab-grown meat sector has high growth potential but is finding it difficult to scale up in the UK regulatory environment. The government could create more special channels through the Regulatory Innovation Office for supervising specific companies or sectors that are deemed to have the potential for high growth and social value.

In other sectors, the existence of rip-off companies encourages an unproductive race to the bottom, incentivising companies to get better at manipulative sales techniques, rather than improving their productive or cutting costs. The Business and Trade Select Committee’s inquiry into ‘Rip-off Britain’ was followed by a CMA crackdown on online pricing practices, such as drip-pricing and hiding costs during the checkout process.23 This is an example of how stronger regulation results in better results for consumers and the market as a whole.

Productive reallocation

While industrial strategy is important for directing the future sectoral composition of an economy, we should not confuse it with a growth strategy.

Indeed, in recent history, productivity increases have come not from jobs moving between sectors but from people moving within them: within-sector reallocation. As Soumaya Keynes writes in the Financial Times: ‘in the US, the EU and the UK, most of the productivity slowdown in the 2010s was because of declining productivity within industries’.24

The UK stands out among our peers by having a large tail of low-performing companies. The worst of these are termed ‘zombie firms’ – those that are staying afloat without adding any value. We are already seeing some ‘early and encouraging’ signs of the replacement of these firms.25 The government should support this, making it easier to close firms and reallocate their staff and resources to more productive enterprises.

Much more work is needed to better understand the reasons behind the problem. One may be the complexity of our tax structure and the cliff-edges within it. It can be very costly for SMEs, for instance, to expand beyond the VAT threshold of £90,000 per year, and so many stay stuck below it.

Tax avoidance is another motivation for individuals. It is more profitable for a highly-paid professional to leave their company’s payroll, and to set up a private company that they restructure their income into, to pay a lower rate of Capital Gains Tax compared to Income Tax. This is commonplace in the professional services and IT sectors.

Similarly, in other sectors, workers may leave firms and set up as sole traders to avoid paying National Insurance Contributions (NICs). However, an IT consultant or a brick-layer may well be less productive trading on their own than inside a company that manages their diary, clients, orders, projects, advertising, and finances for them. Their decision to exit their firm is not rooted in economic efficiency, but in making the best out of a bad tax system. We must change the incentives so that workers and business managers don’t have to face such poor trade-offs.

Conclusion

We have to be honest: laying the foundations of long-term growth through obvious, consensus-based long-term measures is vitally important. But it will not necessarily yield results within the lifetime of this Parliament. For example, take the Resolution Foundation’s Economy 2030 Inquiry, which began in 2020, sought to find measures to progress to end the stagnation already present in the economy before the pandemic.26 The timespan of its measures, capturing the broad consensus of economic views, was over a decade.

Therefore, in addition to building the foundations, we also need short-run approaches to growth: ones that unleash the productive capacity that is already latent in the economy, but are being held back by poor incentives and a lack of state capacity. In order of timing, we can increase the dynamism of our markets; unleash the right kinds of private and public investment; free up more labour supply; and train workers better to withstand long-term transitions.

Yuan Yang has been the Labour MP for Earley and Woodley since 2024

Notes

- Ana Margarida Fernandes and Tristan Reed, Industrial Policy for Development, World Bank Group, March 2026.

- Carsten Jung, Budgeting Better, Institute for Public Policy Research, October 2024.

- George Dibb and Carsten Jung, Rock bottom: Low investment in the UK economy, Institute for Public Policy Research, 18 June 2024.

- Ibid.

- Simon Jäger, Benjamin Schoefer, and Jörg Heining, Labor in the Boardroom, National Bureau of Economic Research, November 2019.

- Ibid.

- Resolution Foundation & Centre for Economic Performance, LSE, Ending Stagnation: A New Economic Strategy for Britain, Resolution Foundation, December 2023.

- Arun Advani, Andrew Lonsdale and Andy Summers, Reforming Capital Gains Tax: Revenue and Distributional Effects, CenTax, October 2024.

- Treasury Committee, National Wealth Fund, UK Parliament, 28 October 2025.

- Jaya Sood and Theo Harris, Firing up the fund, New Economics Foundation, 19 March 2025.

- Ezra Cohen and Matthew Stubbs, Rates and Wrongs: Fixing UK Tax Cliff Edges and Tapers, Centre for British Progress, 25 March 2026.

- Economic and Fiscal Outlook, The Office for Budget Responsibility, March 2023.

- ‘How to apply for 30 hours government funded childcare for working parents and find out if you’re eligible’, www.educationhub.blog.gov.uk, 1 September 2025.

- Hari Menon, Childcare in the UK: Inefficient or underfunded?, Social Market Foundation, 19 October 2023.

- Ibid.

- Francisca Ladouch, UK paternity leave, limited and unequal, Joseph Rowntree Foundation, 16 March 2026.

- Maya Oppenheim, ‘‘Not just broken but elitist’: UK’s top earners benefit most from shared parental leave;’, The Independent, 2 December 2024.

- Louise Woodruff, Improving Statutory Paternity Leave would benefit families and the economy, Joseph Rowntree Foundation, 29 April 2025.

- Tom Pollard and Tom Stephens, The universal family childcare promise, New Economics Foundation, 31 July 2025.

- Iain Porter and Sam Tims, Protected minimum floor in Universal Credit: new policy targeting hardship, Joseph Rowntree Foundation, 9 October 2025.

- Hilary Cottam, Radical Help: How we can remake the relationships between us and revolutionise the welfare state, Virago Press, 2018.

- Mike Brewer and Louise Murphy, From safety net to springboard, Resolution Foundation, September 2023.

- Competition and Markets Authority, ‘CMA launches major consumer protection drive focused on online pricing practices’, www.gov.uk, 18 November 2025.

- Soumaya Keynes, ‘Would a ‘mild zombie apocalypse’ be a good thing for the UK economy?’, Financial Times, 15 January 2026.

- Ruth Curtice and Greg Thwaites, New Year Outlook 2026, Resolution Foundation, 5 January 2026.

- ‘The Economy 2030 Inquiry’, www.economy2030.resolutionfoundation.org.