Published 12/05/2026

Similar crises, different times

Our country’s economy, weakened by a recent crisis, is being plunged into another. Families are struggling; those who can save are anxiously doing so. The resulting lack of demand limits overall economic growth.

At the same time, a war caused by foreign powers is pushing up the price of energy and everything else. As prices continue to rise, the Bank of England is tempted to keep interest rates high, so that homeowners face higher mortgage payments for longer. As a result of these factors and global instability, the government’s cost of borrowing is high – and volatile.

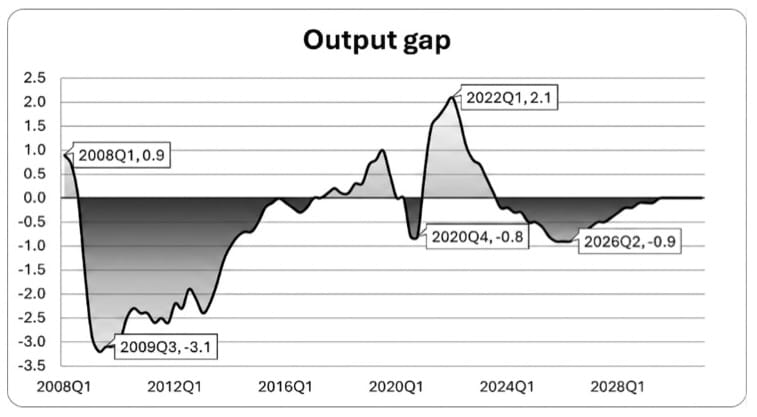

We have been here before – too many times. In 2010, the economy’s lack of demand became a drag on growth, as Conservative and Lib Dem austerity made people poorer. (In economic jargon, the ‘output gap’ widened.) In 2021, the pandemic’s breakdown of global supply chains started sending inflation up, and in 2022, Russia’s invasion of Ukraine spiked energy costs across Europe.

Today, we are now facing all of these crises at the same time. The easier solutions we could’ve tried, had we been in power back in 2010 or 2021, are no longer the right ones for us now. Our response has to include an awareness of the different times we are in and the high cost of debt.

We have to bear down on the cost of living and give households the resilience they need to feel they can spend again, lowering the UK’s unusually high rate of precautionary savings post-Covid.

But we cannot tackle the cost of living without tackling costs. Fiscal subsidies alone will not work: we need to improve the supply side. To do so, we need a productive state that has the ability to lower costs, for example making energy cheaper for businesses as well as households.

Although it’s impossible to fully detangle the two, in this chapter I will focus on households; in my following one I will focus on the wider economy.

Why is demand low – and why is that an issue?

The Government has already taken a number of steps in the November 2025 Budget to cut the cost of living: lowering energy bills for all by around £120, in addition to extending the £150 Warm Homes Discount for six million low-income households; uprating benefits and pensions, freezing the bus fare cap, and freezing rail fares.

Yet despite those measures, the current Parliament is still set to be the worst on record for disposable incomes; even before the Iran war the average family was set to be more than £500 a year worse off at the end of the Parliament than they are today.1

There are two causes of the affordability crisis: incomes have lagged and bills have soared. According to the Institute for Fiscal Studies (IFS), median incomes grew by just 6 per cent between 2009/10 and 2022/23 – compared to 30 per cent before the Great Recession.2 This stems in part from poor productivity growth. In the 2010s UK labour productivity grew by an average of just 0.6 per cent.3

Amongst the poorest fifth of households, the median income was no higher in 2023/24 than it was 19 years previously.4 By January 2026, the standard allowance of Universal Credit was around its lowest ever level as a proportion of average earnings.5. More cuts are baked into the system after 2026, such as nominal freezes to Local Housing Allowance and the benefit cap.6

On the other side of the ledger, bills have soared. This is not only true of our current net imports – food and energy – where we have been subject to global instability. It is also true of our homegrown industries, such as water, housing, and childcare.

The Government has rightly made tackling the cost of living its top priority. The Prime Minister has said that ‘every minute we focus on anything other than cost of living is a wasted minute’. Without serious action to improve livelihoods, the Labour Party is unlikely to win a majority at the next election.

But the affordability crisis is not just an electoral problem – it is an economic one. Demand deficiency is keeping growth low right now, and will continue to do so well into 2029 according to the Office for Budget Responsibility’s (OBR) model.

Demand deficiency is not only caused by the current affordability crisis. Longerterm structural shifts in the economy have also led to lower demand. An ageing population with growing income inequality will spend less of its income. This is what economists in the early 2010s termed ‘secular stagnation’.

By now, British household consumption has been depressed for the best part of two decades.7 Our high level of precautionary savings comes from a longer-term anxiety about our economic futures. It will be difficult to change people’s outlooks. It will take not only strong action, but also strong communication of that action, to give people confidence in the future.

Tackling affordability is not just important for raising demand. An economy in which workers and families feel insecure is an economy that will fail to generate the dynamism and productivity it needs to spur growth.

On the supply side, more secure households are also more likely to be productive at work, more likely to start a business, and more insulated from external economic shocks – all of which supports better labour market turnover and job matching, which in turn generates economic growth. The foundation of a resilient economy is resilient households.

What can we do?

The cost-of-living measures taken at the 2025 November Budget were important first steps. If we were not facing a war in Iran, these measures would’ve brought inflation back to target by April. But the world has changed, yet again. We need further action to bring down inflation, encourage further interest rate cuts and to speed up the economy.

Drawing on the criteria used in my work with the Living Standards Coalition of Labour MPs, the interventions below are progressive, benefitting the median family and the poorest families more than the richest, proportionally to their incomes; immediate, in that impacts can be felt within months; and cheap, in that they can be implemented in a way that is either fiscally neutral, or close to.

The goods and services below were chosen on the following criteria. The biggest costs facing households – housing, transport, food, and childcare for young families – deserve our attention, as well as the unavoidable costs of utilities. We should be doubly focussed on costs that also affect labour market supply, such as childcare, transport, and housing.

Finally, we should be attentive to costs that are unusually high in the UK compared to our peers, such as childcare, as well as costs that have become unusually sticky components of the UK’s inflation mix, such as food. (Since childcare affects labour supply, I will cover it in my second chapter.)

Utilities

Any discussion of the future of water and energy has to reckon with the consequences of the privatisation of utilities. Far from unleashing the market forces of competition, the attempt to create artificial competition in the water sector has led to toothless bureaucracies, low investment, and high costs.

While there is no quick route back to undoing privatisation, it is important we acknowledge its ongoing costs in order to better conceptualise the trade-offs of potential solutions, ranging from nationalisation to setting up public corporations that own assets and issue debt in their own name.

For instance, consider the premium cost of private debt compared to public debt. The rate of interest that Thames Water pays on some of its recent corporate debt is 9.75 per cent, much higher than even the relatively high rates the government pays on its own debt.8

As a result, £28 out of every £100 that households pay Thames Water towards their bills is used to pay back the interest on the company’s debt owed to private creditors.9 In practice, customers rarely draw the distinction between the costs they face: they see the government as broadly responsible for the cost of customer bills, the cost of taxation, and for the water industry’s failures.

The Government’s arms-length regulators are responsible for overseeing every aspect of the water industry; yet they have historically regulated without consideration of consumer cost, and have little power to enforce change that residents can feel. This a prime example of the toothless, unproductive state.

The Government should be less cautious about using Special Administration Regimes (SARs) to deal with spiralling utility companies, as it did in the case of the energy company Bulb. These are the only form of corporate restructuring that take consumers’ interests into account alongside creditors’.

Energy tariff s and energy market reform

The IMF has warned that the UK is uniquely vulnerable among our rich-world peers because of our over-exposure to gas. Our aim should be to make domestic energy prices lower and more stable, as an essential input for both households and businesses.

In response to our current energy crisis, we cannot repeat the Conservatives’ costly mistakes from 2022. The Chancellor is right to take a targeted approach and to support the worst off, rather than to borrow to bail out the wealthy at the expense of mortgage holders and future taxpayers.

Any subsidy to the system will amplify the poor design of energy pricing; therefore the Government should fix this alongside any fiscal measures. It is no coincidence that many European countries changed their energy pricing mechanisms following the 2022 crisis.

Fixed fees such as standing charges are part of what makes the system regressive. The poorest households consume the least energy but pay the largest proportions of their income on their energy bills.

A progressive energy pricing system would lower bills for the poorest households while maintaining incentives to reduce energy consumption among higher energy users. The Government could follow Austria and others in guaranteeing a minimum essential amount of cheaper energy.10

It could then make it increasingly more expensive to buy more energy, in the form of a ‘rising block tariff’.11 This is not particularly radical. In fact, the majority of the world’s population is covered by such a tariff.12 The costs of such policies could thus be redistributed within the bill-payer base, as well as through subsidy.

The Government should also continue down its existing path of removing policy costs from electricity bills and adding them to general taxation. If applied to all policy costs, this would cost £3bn and cut household energy bills by an additional £106.13 If the Government uses taxation in this way, it should also retain equity in the infrastructure it funds, so as to eventually be able to return a profit to the taxpayer.

At the same time as lowering prices, we need to reduce the volatility of prices, which in turn will help with the target of reducing overall inflation. The

Chancellor’s recent decision to break the relationship between gas and electricity prices through issuing contracts that stabilise prices is an example of an intervention that does both.

Institutional obstacles remain. The National Energy Systems Operator (NESO) reports that 283 GW of electricity generation and storage projects await grid connections. That is almost three times the existing generation and storage capacity the UK has in total and twice what the UK needs to achieve its goal of 95 per cent clean power generation by 2030.14

NESO considers these wind, solar, battery and hydrogen storage projects ‘readyto-build’. At the same time, the Department for Energy is currently consulting on how to best prioritise its backlog of connections for projects that consume energy, such as housing developments and manufacturing.15

Arms-length organisations like NESO need state interventions when they are failing, since the end-users of a failing energy system will blame the government for its failures regardless of who operates it.

Transport

While the Government’s freeze on rail fares is a welcome intervention for intercity travellers, the vast majority of public transport journeys are taken by bus, particularly for low-income commuters.

In 2022 IPPR said that free buses for under-25s and people on Universal Credit would cost £0.5bn. Alternatively, capping bus fares for everyone in England at £1 would have cost up to £0.9bn. Both these options are progressive, as even universal interventions that reduce bus fares create disproportionate savings for the lowest income households.16

Food

In the five years since the start of the pandemic, food prices increased by 37 per cent, significantly higher than overall UK prices overall. Since 2023, food inflation has also been persistently higher than comparable European economies, due to Brexit trade frictions and Britain’s higher energy costs.17

Not only are too many British families in food poverty, food prices are also economically important because they have the strongest influence on people’s expectations of inflation.18 Like energy costs, this issue has become even more salient since the war in Iran. Around a third of global fertiliser usually passes through the Strait of Hormuz.19

The Government is already taking steps to improve our economic relationship with the EU, and is poised to agree sanitary and phytosanitary and veterinary deals later this year.

A bespoke customs arrangement would remove the need for rules of origin checks, which could further bring down costs. These moves could feed through to prices by 3-6 per cent by 2030 depending on the depth of alignment.20

While supermarket margins remain thin, the big differentials in the kinds and prices of good stocked by corner shops and small ‘express’ versions of supermarket chains hurts families who don’t live close to budget stores, or whose working patterns mean they shop at unusual times of day or week.

In the short run, a liberalisation of some Sunday trading laws – taken together with the Government’s roll-out of Employment Rights Act protections for workers – will help. In the longer run, planning reforms can help bring more budget stores to every town centre.21

We also need to consider how consumers feel about their shopping experience. This is best summed up as ‘rip-off Britain’. Shoppers have seen shrinkflation, loyalty cards, and misleading pricing as tricks that are being used to squeeze them even more. It is important for the Competition and Markets Authority to be able to speedily discipline the sector when needed, improving the confidence of consumers.

Property management charges

In the property management sector, a lack of regulation has led to the emergence of rogue actors who benefit from a captive audience and no effective scrutiny.

Roughly one in six families in England live in leasehold homes, and thus pay service charges, while an additional proportion are freeholders in estates built in the last two decades, which face estate charges. Between 2018 and 2023, ‘80 per cent of the freehold properties built by the 11 largest housebuilders […] are likely to be subject to such charges’.22

The number of households affected is likely in the millions. Such households are an important part of Labour’s electoral coalition of young, aspirational families. Their satisfaction provides an important test of the government’s promise of new-build homes to address the housing shortage.

These management fees are often charged without transparent accounts, and it is very different to change one’s property manager. In 2024, the average annual service charge bill had increased by 11 per cent to £2,300 – four times the rate of inflation for the same period.23 The average service charge amounted to more than the average cost of all utilities (energy, water and internet) put together.

The Government could consider publishing a reference cost index for the major components of property fees, and cap fee increases to a band around the reference cost. This can be a stop-gap solution while residents are being transitioned into a legal framework that enables them to easily choose their property manager, or until a regulator is set up to enforce residents’ rights.

Fiscal constraints and political economy

Even if the measures in this chapter did the best they possibly could, and fully closed the output gap, we would still only reach a disappointingly low-growth equilibrium.

In its Autumn 2025 forecast, the OBR finally downgraded its expectations for growth by an average of 0.3 percentage points for 2026 to 2029. This decision came because of weak productivity growth since the financial crisis, which has been explained in several ways, including the years of economic scarring from the 2010s – ‘where productivity takes longer to recover after workers experience persistent unemployment or firms delay investment’.24

If prolonged low demand can scar an economy permanently, then could high excess demand heal those scars? In other words, should the UK follow in the footsteps of the early 2020s Biden administration, and run the economy hot?

The majority of interventions discussed above are fairly cheap, particularly compared to the impact they offer. Taking more dramatic action requires more government spending. There are sharp trade-offs to going further by spending more. Yet the shape of these trade-offs is not fully foreseeable in advance.

The US invasion of Iran will lead to more unexpected price shocks that last an unpredictable amount of time. The global economy is already overheated – which leaves little room for us to apply the heat domestically through raising demand above equilibrium – even if we could.

To escape our low-growth equilibrium, we have to address the structure of regulation, ownership and tax incentives in the wider economy, which I will discuss in my following contribution.

Yuan Yang has been the Labour MP for Earley and Woodley since 2024.

Notes

- Sam Tims, Chris Belfield and Camron Aref-Adib, Weak income growth leaves people with little resistance to shocks, Joseph Rowntree Foundation, 15 April 2026.

- Jonathan Cribb and Tom Waters, Past 15 years have been worst for income growth in generations, Institute of Fiscal Studies, 31 May 2024.

- Simon Pittaway, Yanked Away, Resolution Foundation, April 2025.

- Sam Tims, Chris Belfield and Peter Matejic, A decade of falling incomes?, Joseph Rowntree Foundation, 25 September 2025.

- Trussell and Joseph Rowntree Foundation, ‘Guarantee our Essentials: reforming Universal Credit to ensure we can all afford the essentials in hard times’, www.jrf.org.uk, 30 January 2026.

- Alex Clegg, Louise Murphy and James Smith, Living Standards Outlook 2026, Resolution Foundation, February 2026.

- Consumer trends, Office for National Statistics, 31 March 2026.

- Robert Smith, ‘Thames Water £3bn rescue loan gets High Court approval’, Financial Times, 18 February 2025.

- Analysis presented in Carmen Aguilar García, Anna Leach and Sandra Laville, ‘Water firms use up to 28% of bill payments to service debt in areas of England’, The Guardian, 18 December 2023.

- Chaitanya Kumar, Isabel Bull and Alex Chapman, Protecting consumers and the UK economy from an energy price shock, New Economics Foundation, 9 April 2026.

- Alex Chapman and Chaitanya Kumar, A long-term policy to protect essential energy needs, reduce bills and cut carbon, New Economics Foundation, March 2023.

- Alex Chapman, Outside Europe it’s normal to protect basic energy needs – so why don’t we?, New Economics Foundation, 22 August 2024.

- Chaitanya Kumar, Isabel Bull and Alex Chapman, Protecting consumers and the UK economy from an energy price shock, New Economics Foundation, 9 April 2026.

- National Energy Systems Operator, ‘NESO implements electricity grid connection reforms to unlock investment in Great Britain’, www.neso.energy, 8 December 2025.

- Department for Energy Security and Net Zero, ‘Accelerating electricity network connections for strategic demand’, www.gov.uk, 12 March 2026.

- Stephen Frost, Luke Murphy and Shreya Nanda, To support low-income households, it’s time to reduce to the cost of daily bus travel, Institute for Public Policy Research, 6 October 2022.

- Dr Liliana Danila, UK Food & Drink Inflation 2025-26, The Food and Drink Federation, September 2025.

- Nikoleta Anesti, Vania Esady and Matthew Naylor, Food prices matter most: sensitive household inflation expectations, Bank of England, May 2025.

- UN Trade and Development (UNCTAD), ‘Hormuz shipping disruptions raise risks for energy, fertilizers and vulnerable economies’, www.unctad.org, 10 March 2026.

- David Lawrence, Kane Emerson and Yuan Yang, Ways to reduce food prices before 2029, Centre for British Progress, 12 February 2026.

- Ibid.

- Housebuilding market study, Competition and Markets Authority, 3 November 2023 23. Hamptons, ‘Service Charge Index 2024’, www.hamptons.co.uk, February 2025. Forecasting Productivity, Office of Budget Responsibility, November 2025.